Two weeks have passed since the finalisation of 2025 copper concentrates long-term contracts, and negotiations for long-term contracts in the US dollar copper market are also in full swing. Following intense negotiations last week, upstream and downstream enterprises have gradually finalised long-term contracts this week. Based on certain exchanges, SMM has analysed and summarised the current progress and partial results of long-term contract negotiations in the US dollar copper market as follows.

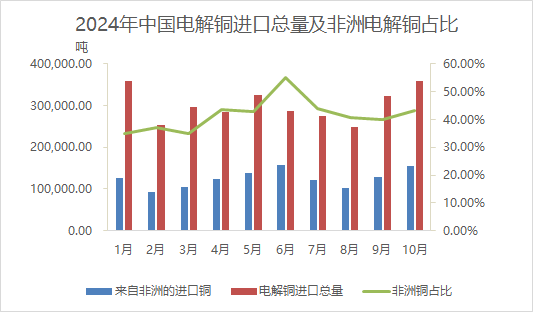

Africa is an important source region for China's copper cathode imports. From January-October 2024, copper cathode from Africa accounted for over 40% of the total copper cathode imports, nearly half of the total. The EQ long-term contract negotiations in the US dollar copper market have also commenced. According to SMM's analysis, the 2025 EQ long-term contracts CIF Shanghai are fully fixed, with the center in the $5-8/mt range, QP as M+1. A small number of enterprises can sign contracts in the $0-5/mt range, QP as M+1. Overall, this represents a decrease of $5-10 compared to the 2024 long-term contract levels. Additionally, local African copper miners are actively tendering, but the offers are quite varied. FCA mainly includes the following three tiers: ① (-490) to (-495) $/mt, QP M+3; ② (-470) to (-475) $/mt, QP M+2; ③ (-450) $/mt, QP M+1. However, as some enterprises have not yet started tendering, SMM will continue to monitor the subsequent developments.

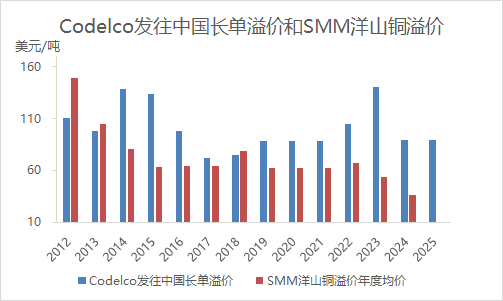

Regarding registered copper, overseas smelters have made rapid progress in signing first-hand long-term contracts this week. The 2025 long-term contract offers are mostly consistent with those of 2024 (Codelco's first-round offer to Chinese enterprises was $89/mt, pricing month M+1; LS's first-round offer to Chinese enterprises was $70-73/mt, pricing month M+0). Buyers sought to counteroffer with lower prices, but overseas smelters remained firm, ultimately concluding deals at the offered prices. Meanwhile, long-term contract negotiations among traders are also underway but progressing relatively slower. It is understood that downstream parties prefer to sign contracts with floating prices, and upstream offers have been adjusted accordingly. Semi-fixed and semi-floating, as well as fully floating models, are present, but they require acceptance of a minimum limit of $35/mt, with some requiring the inclusion of domestic warehouse warrants without brand restrictions. Floating benchmarks are mostly based on SMM monthly averages, with an upward adjustment of $3-5. Fixed portions for mixed pyrometallurgical methods are offered at $60-70/mt. For near-sea sources, QP is the shipment month M+1/M+0, while for distant-sea sources, QP is the shipment month M+2/M+1.

Overall, first-hand long-term contracts from overseas smelters were mostly signed at the offered prices, while the proportion of floating contracts among traders has increased, with more flexible and diverse signing methods. The market is still under negotiation. SMM will continue to follow up on the progress of 2025 US dollar copper market long-term contract negotiations.